Global events can cause uncertainty in markets, which sometimes reflects in your super balance. If you’re close to retirement, or already retired, this can feel unsettling and raise questions.

We share our responses to some commonly asked questions.

Why is my super balance going down?

Most super fund investment options invest in Australian and overseas shares. When the value of these shares is impacted by major events in Australia or around the world, you might see the result in your super balance.

Market volatility is a normal part of investing. History tells us that, over longer periods of time, markets generally recover after major events.

For many members, super remains invested even after they’re retired and are withdrawing an income from their account. That’s why it’s important to avoid hasty decisions in response to market volatility.

Should I take all my money out of super when the market drops?

If you’re eligible to access your super, you might be tempted to withdraw it to stop your balance falling any further. This can be a risky thing to do, because you might miss out on the potential growth that can come when markets readjust.

For example, let’s say your super balance was $175,000 and then it dropped to $150,000 due to market volatility. If you withdraw that $150,000, you risk ‘locking in your losses’ because if the markets recover strongly your super could rebound to its previous balance and potentially grow even more.

There can still be reasons to withdraw money from your super depending on your personal circumstances, however it’s important to make sure you understand the potential impact and think it through before doing anything. You might want to book a call with a Rest Super Specialist too.

Should I move my super to cash?

Most Rest members have their super in the Balanced or Growth option. These investment options invest in a portfolio of growth and defensive assets consisting of shares and debt (both Australian and overseas), property, infrastructure, cash and alternatives.

If you move all your super into the Cash investment option, you won’t be invested in any growth assets. This means you probably won’t see as many fluctuations in your super balance, but you may miss out on higher potential investment returns over the long term.

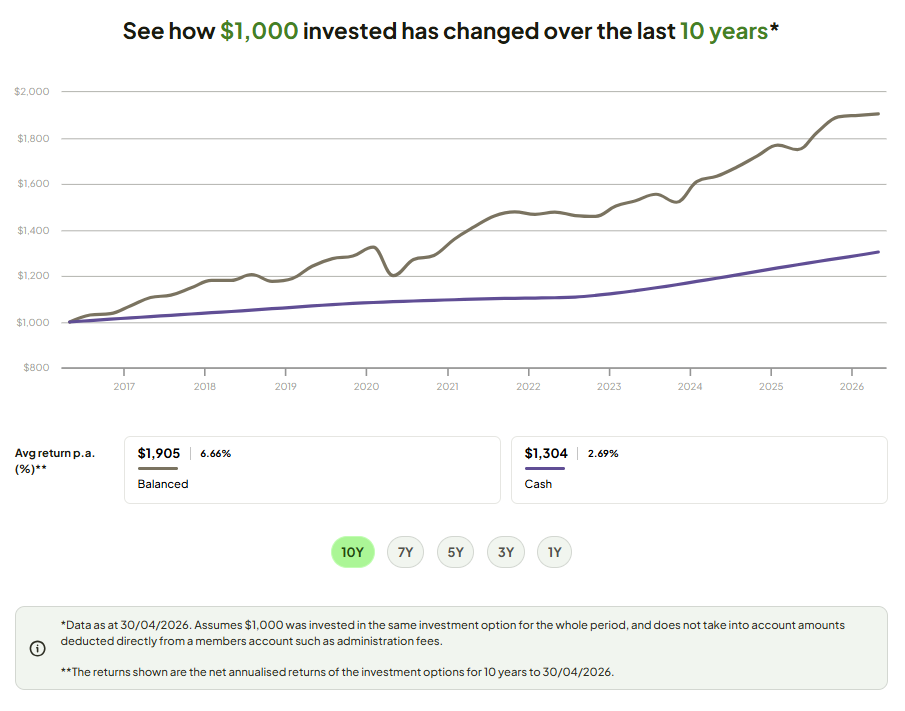

The graph below shows the performance over 10 years for the Rest Pension Balanced and Cash options. As you can see, there are more ups and downs for the Balanced option, but the performance is stronger over time. If you invested $1,000 in the Balanced option on 30 April 2016, it would have grown to $1,905 by 30 April 2026. If you invested it in the Cash option, it would have grown to $1,304.

Source: 10-year investment returns to 30 April 2026 for Rest Pension – Balanced and Rest Pension – Cash investment options. Past performance is not a reliable indicator of future performance. Investment returns are only one factor to consider when deciding how to invest your super.

How is Rest managing my investments?

Our investment team – and the specialist managers we work with – are continuously assessing global risks, analysing market news, and managing portfolios to ensure they are well-positioned. Volatile markets may offer opportunities to buy strong, high-quality investments at lower prices. These opportunities don’t come along often, but when they do, they can help improve long-term returns for members.

We focus on the economic and financial drivers of market returns and aim to use market ups and downs to our advantage when it makes sense.

Should I increase/decrease my pension payments?

If you’re currently taking out more than the minimum and you can afford to live on less for a while, you might want to consider if leaving more of your super invested to give it a chance to recover is right for you. Remember that you have to withdraw a minimum percentage from your pension account each year. This percentage is set by the government. It’s based on your age and account balance on 1 July each year.

If you’re finding it hard to meet your living expenses, increasing your pension payments may help you feel more comfortable financially. Or you can make additional withdrawals on top of your regular payments whenever you want. Keep in mind that this will make your super balance go down faster.

You can change your pension payment amount or request additional withdrawals at any time using MemberAccess or the Rest App. Consider booking a call with a Rest Super Specialist if you need help with your retirement income.

Can I access my super early if I’m struggling financially?

Generally, you can’t access your super until you meet what’s called a condition of release. Turning 65 is one of the common conditions of release. Others include leaving an employer or retiring after turning 60.

The Australian Taxation Office (ATO) does allow early access to super if you can prove that you’re experiencing severe financial hardship. You’ll need to meet certain conditions, such as receiving eligible government income support payments.

Use our early access to super tool to see if you might be eligible.

How can I apply for the Government Age Pension?

If you’re 67 or older, and you meet the eligibility requirements, the Government Age Pension can form part of your retirement income alongside your super. You have to be an Australian resident and your income and assets must fall below the limits set by the government.

Age Pension payments can be up to $1,100.30 per fortnight for a single person, or $829.40 per fortnight for a couple (per person).*

If you think you might be eligible but you haven’t applied yet, try out the free Retirement Essentials Age Pension eligibility calculator. The calculator will help you work out if you’re eligible for the Age Pension and provide an estimate of how much you can get. Retirement Essentials can also assist with your Age Pension application (for a fee).

What other financial support is available from the Australian Government?

On top of the Age Pension, you may be eligible to receive concessions and financial support such as the Commonwealth Seniors Health Card, Pensioner Concession Card, Pension Supplement, and Rent Assistance. Check the Services Australia website for details.

Who can I talk to?

If you’re concerned about your retirement savings, we recommend booking a call with a Rest Super Specialist before making any changes. They can help you understand how market volatility impacts your super and answer any general questions you might have. They can also book a call with a Rest Adviser if you need personal advice, who can support you with tailored strategies based on your personal situation, timelines and goals. The adviser can then talk to you about your personal circumstances and help you decide on the best course of action.

* The Department of Social Services adjusts these rates every 20 March and 20 September. The amounts shown are the maximum rates each fortnight as at the date of this article.