Our default option, Growth, returned 9.85% over the 2025 financial year and our default pension option, Balanced, returned 9.21%.

Returns (%)

1 year

10 year p.a.

20 year p.a.

Since inception p.a.

Growth (Super)

9.85

6.78

7.30

8.33

Balanced (Pension)

9.21

6.20

6.92

7.42

Source: Rest, 30 June 2025. Returns are net of investment fees and tax, except Pension, which is untaxed. The earnings applied to members’ accounts may differ. Investment returns are at the investment option level and are reflected in the unit prices for those options. Returns for periods greater than one year are annualised. Past performance is not an indicator of future performance. Inception dates are 1 July 1988 for Growth and 13 September 2002 for the Balanced (Pension) option.

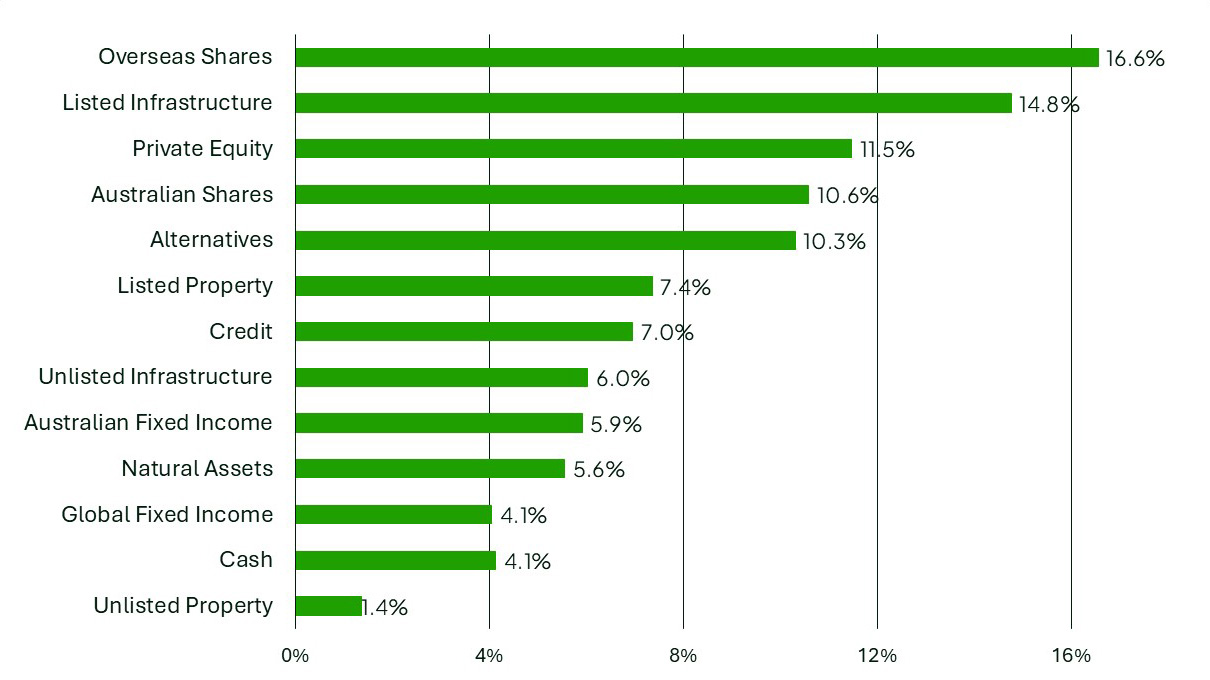

A number of Rest’s investment options also delivered double digit returns last year:

For Rest’s Growth option, Overseas Shares, Listed Infrastructure and Private Equity were the top performers, and all asset classes delivered positive returns.

Growth asset class returns FY2025

Source: Rest, 30 June 2025. Returns are net of fees and tax and based on unit prices. Past performance is not an indicator of future performance.

Looking back…

Share markets led returns upwards despite volatility

Despite a backdrop of geopolitical upheaval and policy challenges resulting in volatile market conditions at times, shares continued to be a significant return contributor overall for the third consecutive year.

Global share markets performed strongly overall. Whilst the US share market made up a large proportion of the return, other major share markets also performed well. In the US, the big brand technology and consumer stocks led the charge again over the first eight months, delivering around 30% of the market return. The buoyant US market was largely led by a supportive macro-economic environment, which translated into strong company earnings overall.

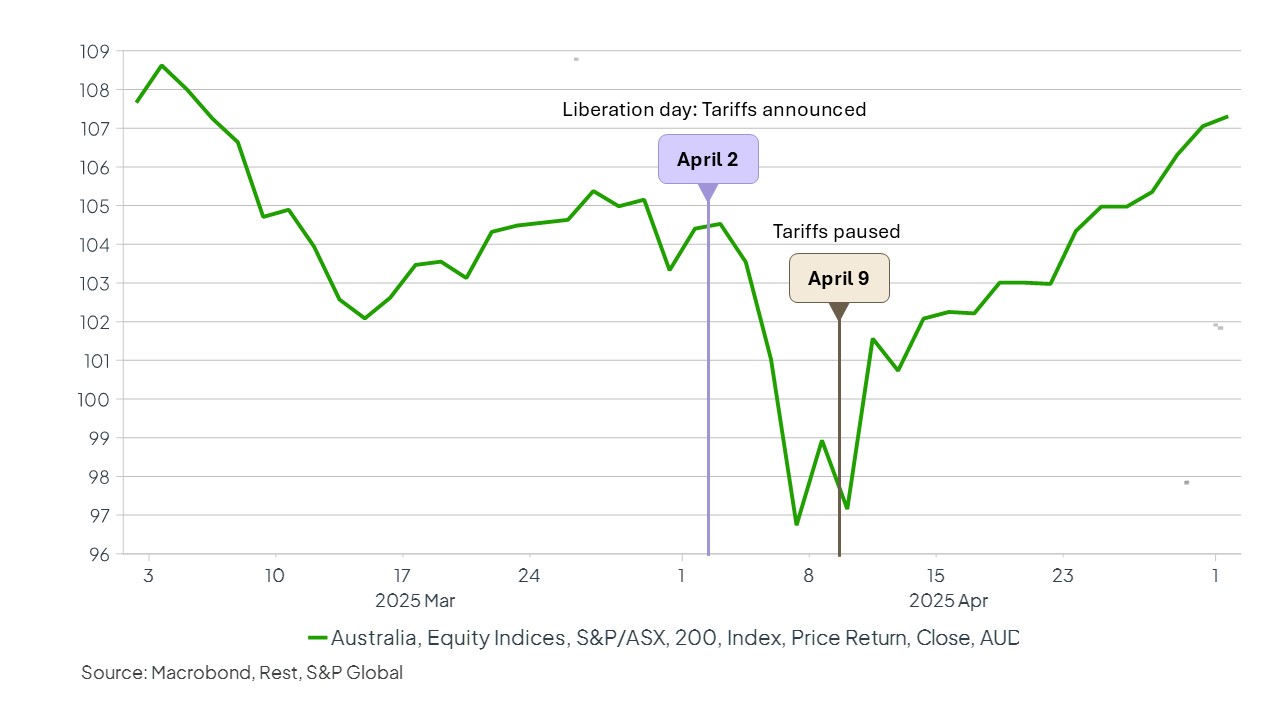

This strength in major share markets continued through to mid-February, before the market pulled back as US government tariffs were announced in early April. President Trump’s “trade wars” unsettled global markets as pricing impacts flowed through to companies, causing heightened volatility, especially across share and bond markets. Despite the volatility, major share markets recovered quickly.

The ASX200 in March and April

The Australian share market was no exception. For example, we can see in the graph above that the ASX 200 (one of the main Australian shares indexes) plunged 7.5% over a few days in April following Trump’s announcement of the tariffs. The market then rallied 10.7% from the low, returning 3.6% by the end of the month. By mid-June, the Australian share market and other major global markets were again passing record levels as conditions remained favourable for economic growth.

In the Australian share market, the financial sector, especially banks, outperformed amidst signs of inflation moderating and employment conditions improving. Australian shares delivered their best return in four years, led by the Commonwealth Bank (CBA) which made up a massive ~30% of the market return, earning itself a witty nickname of the “magnificent one”.

However, just as we headed towards the close of the financial year, further conflict broke out in the Middle East between Israel and Iran. Despite a short-term spike in oil prices, markets again quickly overcame more volatility to finish on a high note.

In the March quarter, Australian growth (GDP) missed the mark slightly, as did employment data. However, over the full year, GDP increased, supported by net positive immigration and employment grew by 2%. Inflation continued to slowly reduce towards the lower end of the Reserve Bank’s long-term goal, which contributed to interest rate cuts in February and May, bringing relief to mortgage holders.

For Rest’s investment options, global economic strength provided a supportive backdrop for investment growth, helping all asset classes deliver positive returns. Infrastructure was also a key beneficiary, with increased global travel benefitting our holdings in airports. A number of Rest’s long standing directly held infrastructure assets also delivered strong returns, especially across energy infrastructure and renewable energy, showcasing the value of investing in quality long term assets. Valuations improved across our property portfolios, with Australian Retail, Sydney Office and Real Estate Credit the main contributors. In fixed income, our overweight tilt to credit contributed positively whilst bond returns were also solid as yields fell, and inflation trended downwards.

Being invested across a range of public and private markets assets helps cushion our portfolios through these challenging times and offers resilience when markets are turbulent. Staying the course and maintaining our long-term investment strategy is also especially important during uncertain periods.

Looking forward

We are generally positive heading into the next financial year however we do expect some economic slowing as the tariff impact starts to flow through and the broader geopolitical backdrop is one that remains highly uncertain.

There’s a strong risk that US government tariffs could cause further disruption to global markets. This could result in further periods of volatility and lower growth expectations in the short term, and shifts in trading patterns over the long term.

The Australian economy is expected to pick up modestly over the second half of the year aided by rate cuts, a pick-up in consumer spending and increased government spending. If inflation continues to fall, we think there is a chance of at least two more interest rate cuts this year, which will help bring relief to mortgage holders.

In an uncertain world, we believe diversification and targeting high-quality assets remains critically important to investing. Our diversified portfolios have remained resilient through difficult environments because of how we invest – with a long-term mindset, a focus on quality and an ability to build well-balanced portfolios.

With Rest’s FY2025 returns across all our diversified options well above our ten-year average annual returns, we are pleased to continue to deliver consistent and strong returns to help you feel secure and confident about the growth of your retirement savings.

Was this page helpful?

Want to learn more?

Investment Updates

How recent global events impact your super

We explain why this happens and what it means for you and your super.