During times of uncertainty, it's only natural to feel both interested and a bit nervous about what’s happening with your hard-earned super.

When it comes to how and where to invest your super, there are many widely-held beliefs and not all are true. We look at some common misconceptions when it comes to investing your super and bust a few of the most common myths.

Myth 1 – Investing in cash is completely risk-free

It’s generally considered low risk to invest in cash (like term deposits and bank accounts), and this can seem like an attractive, safe option. Some people look to invest in cash under the assumption it’s completely risk free. However, cash comes with certain downsides to consider.

Cash investments tend to have low levels of risk and benefit from comparatively high liquidity (i.e. the ability to access your money). Consequently, cash investments typically offer a lower return. If you’re investing for the long-term, investing in cash may expose you to inflation risk and may mean you miss out on potentially higher returns.

Inflation risk

Money has value because it can be used to buy goods and services. And because the price of goods and services tends to go up over time – known as inflation - the real value of a dollar tends to go down over time. The interest earned on cash can be less than the inflation rate. When this happens the real value of the cash in your savings account may go down over time, with the result being that you can afford to buy less than on the day you originally deposited your money. So even if the amount of money in your cash account has increased because of the interest you’ve earned, financially you might have stayed the same or even gone backwards.

Using the price of a takeaway coffee as an example, if inflation has averaged 2.83%1 per year, a cup of coffee priced at $5 currently would have cost $3.78 a decade ago. If we apply the same rate of inflation, that same cup of coffee will cost $6.61 in 10 years, that’s an increase of around 32%. If over that same period the interest earned on cash investments is 2.48%p.a.2, your bank savings account could have grown by less than the rate of inflation.

Potential growth missed?

If you’re investing in cash long-term, you may miss out on the potential growth you could have achieved in riskier assets. For example, if $100k is invested in cash for 5 years rather than in riskier assets like shares, and those riskier assets consistently earn slightly more than what your cash account is earning over time, that difference can really add up over time.

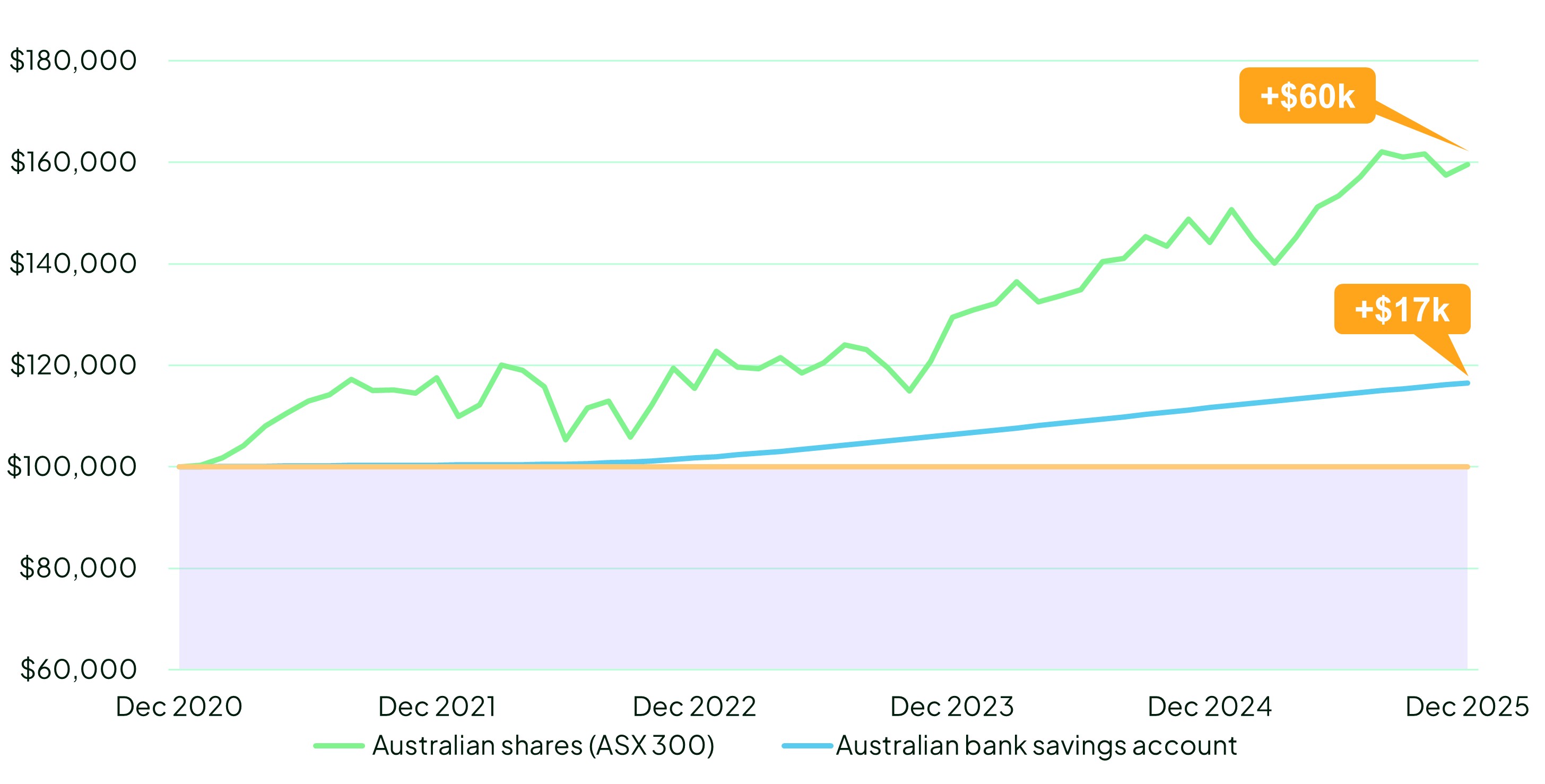

While past performance is not an indicator of future performance, the chart below shows the different experience for someone who invested $100k in Australian shares 5 years ago (the green line) versus someone who invested $100k in cash (the blue line) up to 31 December 2025. The person invested in Australian equities would have experienced some large ups and downs. However, if they were comfortable holding onto their shares for 5 years, they would have earned an extra $43k compared to the person who invested in cash.

What if I invested $100,000 5 years ago?

Source: Bloomberg and the Reserve Bank of Australia (RBA). Australian shares performance is based on the monthly returns for the S&P ASX 300 Accumulation Index from 31 December 2020 to 31 December 2025. The bank savings account uses a monthly time series from the RBA – ‘Banks’ bonus savings accounts. Past performance is not an indicator of future performance.

How market volatility affects your super

You may have noticed your account balance recently fluctuate due to market changes. Learn more about how market volatility affects your super.

Moving to cash temporarily could help your super avoid the short-term market volatility that riskier growth assets sometimes experience. One risk to consider though is that growth assets like shares and property can rebound quickly and without warning after a downturn. Missing that potential recovery could have a negative financial impact over the long-term for your super balance.

Cash can be a useful investment and including a component of cash in your super can provide stability to your portfolio. Depending on your personal circumstances it could even be the most appropriate investment. But make sure you understand your investment options and what the risks are for each. You can speak to a financial adviser to find out more.

Myth 2 - Bricks and mortar is the safest investment

In Australia, property tends to be a popular investment and, as an asset class, it has performed well overall in the past. You can touch and feel property – making it a tangible investment. These factors can give some investors a false sense of security - it might surprise you that property is considered a mid-risk asset.

As you’ve probably heard before, past performance is no guarantee of future performance. Just because property has performed well in the past, doesn’t mean it will do so automatically in the future. As a mid-risk asset, property is subject to a level of volatility and therefore is expected to experience losses at various points in time over the long term.

Property does play an important role in many of Rest’s diversified investment options, but every asset class will go through periods of over- and under-performance. Diversification, which involves spreading your investments across different types of asset classes, is one way to help reduce risk while still allowing your super to grow.

Myth 3 - You should automatically take less risk once you retire

Some people believe that once they retire then it’s automatically time to reduce their investment risk or take very little risk and start living off their accumulated savings. Many of us will enjoy a long retirement though and wouldn’t want to sacrifice quality of life during retirement, so we need to make sure our super lasts. That’s why it’s important to consider taking on the right level of investment risk which is appropriate for your desired retirement plans.

For example, you might decide to start a pension when you retire so that you can receive regular income. In the meantime, the investment option your pension is invested in has the potential to continue to generate returns.

Continuing to take the appropriate level of investment risk could be a factor in:

keeping your retirement savings aligned with the cost of living, which tends to increase over time (due to inflation).

increasing your level of income in retirement, so you can be more comfortable financially.

Rest Advice when you need it

Everyone’s situation is different. So, it’s important that any investment you make is appropriate to you and your situation. You can seek financial advice for help in selecting an appropriate investment option for you.

1. Data as of December 2025. The inflation rate is based on the Consumer Price Index as published by the Australian Bureau of Statistics for 10 years to 31 December 2025.

2. Data as of December 2025. The cash return is based on the Reserve Bank of Australia’s statistics: F4 – Retail Deposit and Investment Rates. The series used is ‘Banks' bonus savings accounts’ which are deposit accounts that pay a higher rate of interest if at least one deposit and no withdrawals are made each month. Figures for ‘banks’ bonus savings accounts’ are an average of the five largest banks’ rates assuming these requirements are met. Series ID: FRDIRSAB10K.

Was this page helpful?

Want to learn more?

General

Risk and return in your super investments

Investments involve risk including super. Learn about risks to consider before investing your super.

Diversification: why is it important for your super?

A simple guide to help you understand the potential benefits of diversification, why it matters to your super and what a diversified portfolio might look like.