The investment timeframe refers to how long you intend to have your money (or super) invested before you need to access it.

When deciding how to invest your super, it’s important to consider your investment timeframe before making any decisions.

Determining your own investment timeframe

While for most people, super is a long-term investment, everyone’s situation is different and that may not be the case for you. Your personal circumstances will influence how long you plan to invest your super (or your investment timeframe), for example:

if you’ve just started working, it may be forty years before you have access to your super;

if you’ve already retired, maybe you plan to spend most of your super to pay off the remainder of your mortgage next month; or

maybe your investment timeframe is somewhere in between.

Keep in mind, just because you’ve retired, that doesn’t necessarily mean your investment timeframe is short. It depends on when you plan to spend each dollar. After all, you might be retired for 30 years (or perhaps even longer!).

Time and volatility

Ever noticed large swings in the value of your super investments? If your super balance tends to change dramatically and unexpectedly over a short period of time, it’s considered to be volatile. These swings in your balance are usually in response to changes in market conditions. High volatility can be a symptom of high-risk investments.

Typically, investments tend to be more volatile over short timeframes, so taking more risk over a short timeframe magnifies this volatility.

If you’re younger and have a longer investment timeframe, some volatility in your investments isn’t necessarily a bad thing. This is because you generally have more time to recover from any losses.

Now let’s say you plan to start spending your retirement savings in 6 months’ time. If you have a short investment timeframe, investing your super in volatile assets may not suit you as you’ll likely want to prevent major losses.

Nearing retirement? Here are some key takeouts to consider:

Try to avoid timing the market: Switching investment options at the wrong time and without advice can lock in losses and risks missing a market rebound.

Diversification: many of Rest’s investment options combine asset classes to help balance risks and smooth returns over time.

Market movements: market changes can take a while to reflect in super balances (both up and down), so impacts may not be immediately visible.

We can help: different strategies are available depending on your retirement stage, so it’s best to have a chat to a Rest Super Specialist.

Investment returns – the relationship between time and volatility

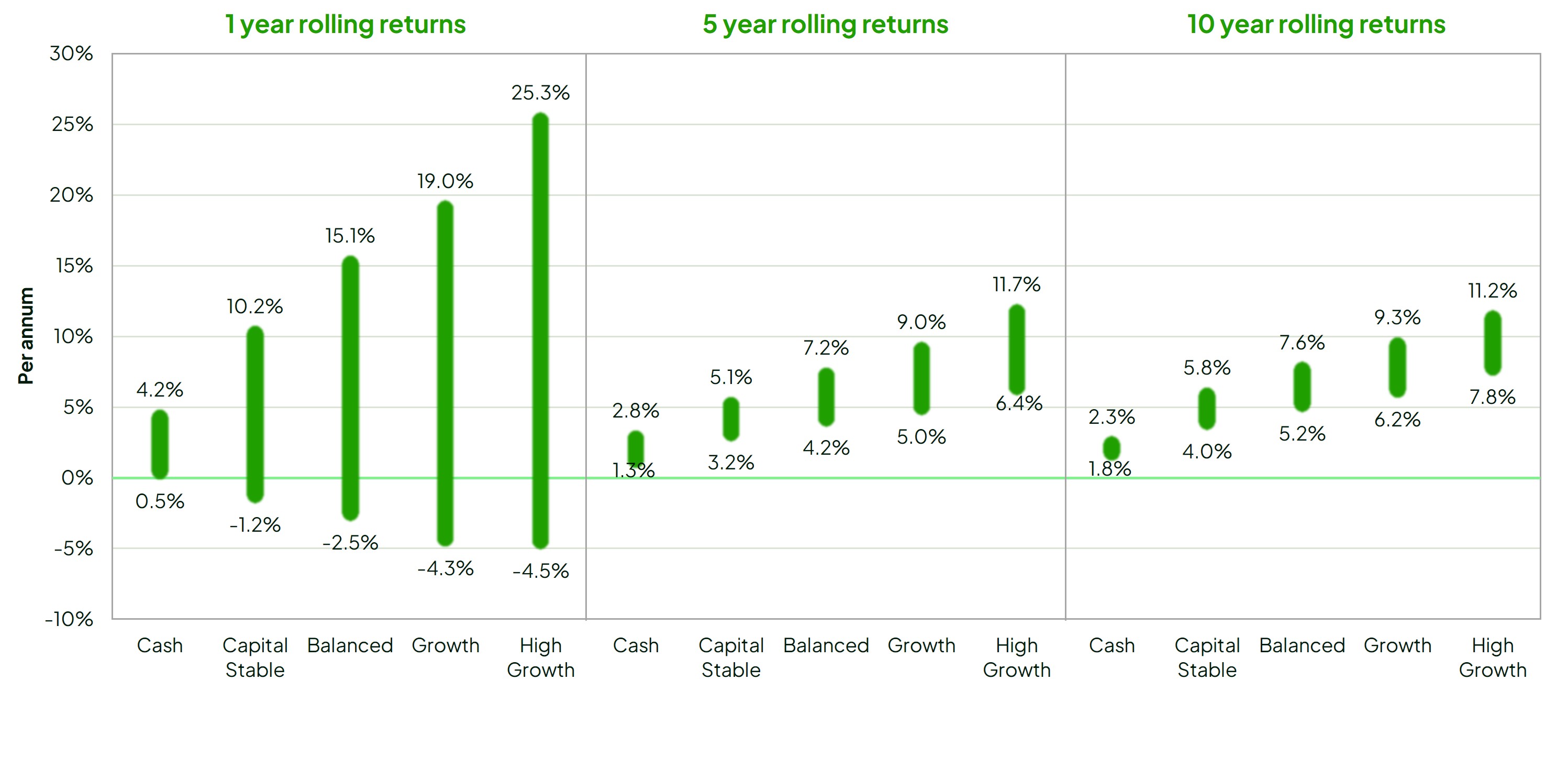

To illustrate the general principle that investments held for a longer timeframe tend to be less volatile, let's examine a range of Rest investment options. The options we have shown below are across a range of risk levels from low to high risk, which are based on the Standard Risk Measure1:

The graph below shows the different rolling returns of these investment options across a range of timeframes and demonstrates the relationship between timeframe and volatility.

Range of returns over time to 31 December 2025

Source: Rest 31 December 2025. Ranges shown in the graph consist of returns over the indicated return timeframes (1 year, 5 year or 10 year), calculated at the end of each month over the period from 31 December 2020 to 31 December 2025. Past performance is not a reliable indicator of future performance.

Looking at the graph, you’ll notice:

Shorter investment timeframes display a greater range of return outcomes, particularly for riskier options (such as Growth or High Growth). Had you invested in the High Growth option for only 1 year, your super balance could have gone down as much as 5% or you may have made a lot of money (as much as 25%!) depending on when you timed your investment.

As the investment timeframe increases, the potential outcomes become less variable.

Generally, shorter investment timeframes exhibit higher volatility and risk. This relationship becomes even more pronounced with riskier investments. That’s why it’s important to carefully consider your investment timeframe before determining the level of risk you're willing to take on.

Consider your situation

When making decisions about how to invest your super, you shouldn't forget about your time to retirement.

Time is only one of many factors to consider when investing. Everyone’s situation and tolerance for risk is different. So, if you are at all unsure which investment option is appropriate, you may wish to seek professional financial advice.

Was this page helpful?

Want to learn more?

General

Risk and return in your super investments

Investments involve risk including super. Learn about risks to consider before investing your super.