The value of your super balance taking a dip. But what’s up today could be down tomorrow, and timing the market is tricky business.

So, while chasing returns (switching into a different investment strategy based on strong recent returns) might seem logical, there are several risks to consider before switching.

Don't rely on past performance

The tried and tested financial disclaimer “past performance isn’t indicative of future performance” is a regulatory requirement in Australia – for good reason. Researching an investment’s performance history can play a part in deciding where to invest your super, but it doesn’t necessarily give you a complete or accurate picture of its future performance.

In 2003, major regulator for the financial services industry, the Australian Securities and Investments Commission (ASIC) commissioned a review1 of over 100 academic studies that look at the predictive value of past performance. One of the conclusions was that:

“Good past performance seems to be, at best, a weak and unreliable predictor of future good performance over the medium to long term. About half the studies found no correlation at all between good past and good future performance.”

There’s bound to be an investment that has recently seen better returns than yours. But there are sound financial reasons why you should think twice before switching.

Why doesn’t past performance count for much?

In other parts of our lives, previous performance is often a strong indicator of future performance. So why isn’t this the same for investments?

It is important to recognise that markets are always changing. The best investment approach at one point in time won’t necessarily be the best approach later. For example, many investors did very well from fast growing tech shares in the late 90s. Huge prices were paid, and values went through the roof, sometimes without much substance behind them. But when it all got too hot, the market “bubble” burst - those who had jumped in too late may have lost a significant amount of money2.

The chart below demonstrates the rise and fall of tech shares by looking at the performance of the NASDAQ Composite. The NASDAQ Composite is an index that tracks the performance of more than 2,500 stocks listed on the NASDAQ stock exchange. Most of these stocks are technology and internet-based companies, and so the index can provide a representation of how tech stocks are performing.

The decline of tech shares in the early 2000s

Source: Rest and Bloomberg, 31 January 2003. Past performance is not an indicator of future performance.

The risks of relying on past performance: an example

Take this example: an investor named Doug kept hearing from his friends about how much money they were making from investing in tech shares. So, at the beginning of the year 2000, Doug decided to jump into the tech share market as one of his new years’ resolutions and invested $50k…Unfortunately for Doug though, the tech bubble was just about to burst. By the end of the year 2000, the NASDAQ Composite had dropped over 40%, meaning Doug would have lost about $20k in one year.

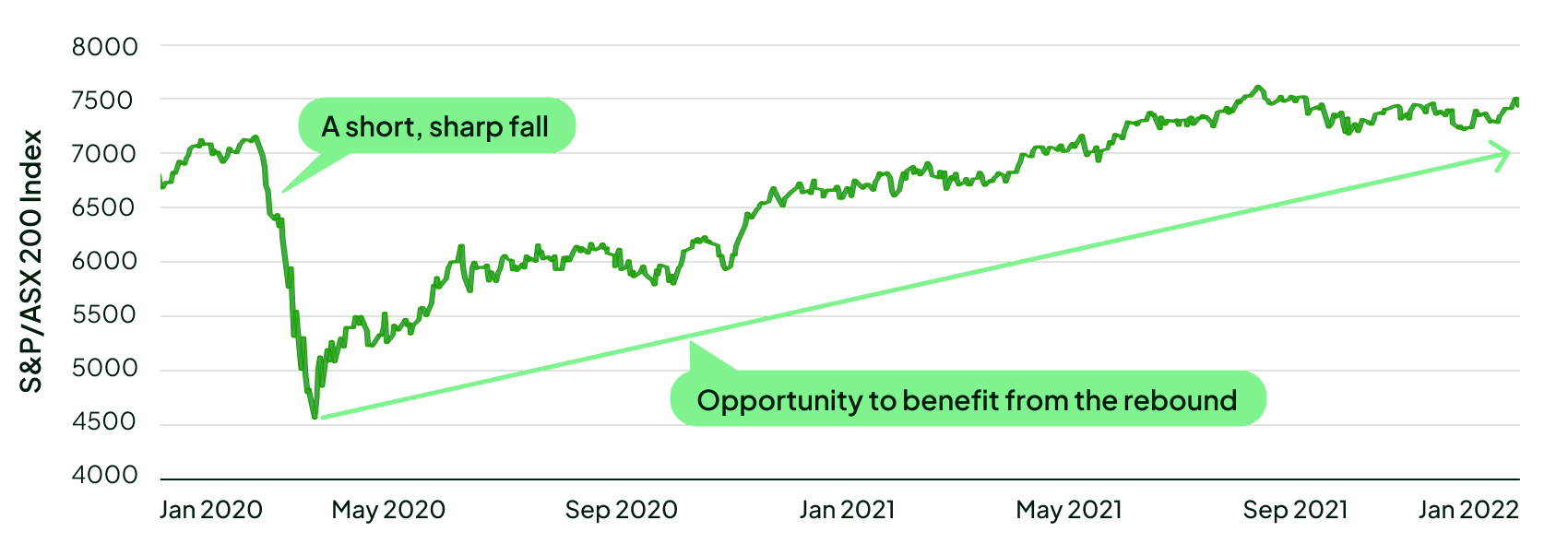

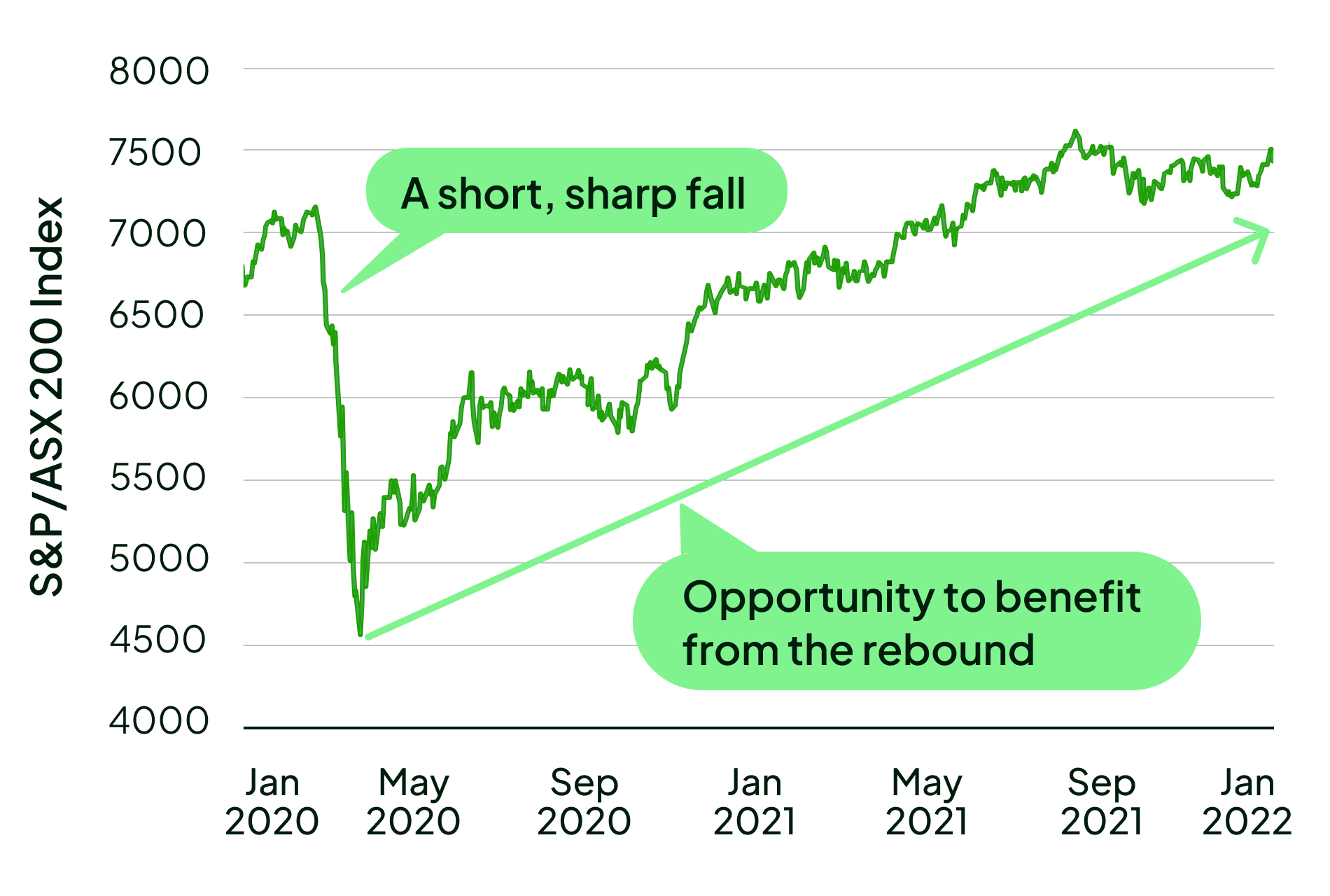

However, you shouldn’t always ignore an investment because of poor recent performance. Markets can rebound quickly, and sometimes, an asset or share that has had a bad run could present an investment opportunity. For example, if you look below, the Australian share market experienced a huge drop over February to March 2020 due to the COVID-19 pandemic. It presented an investment opportunity as it was now much cheaper to buy stocks/shares compared to just one or two months ago.

So if you invested in the ASX 200 on 1 April 2020, you would have enjoyed a 25% return by the end of that year!

Australian shares in 2020: when a downturn becomes an opportunity

Source: Rest and Bloomberg, 2 January 2022. Past performance is not an indicator of future performance.

Thinking of switching? Consider these risks:

1. You risk bad timing

Many investors make mistakes by switching investments too soon when they perform poorly or switching too late when they perform well. 2021 US research3 shows the average investor tends to buy high and sell low which results in worse returns.

2. You pay transaction costs

You’ll likely pay transaction costs each time you switch investments. This is sometimes referred to the buy-sell spread, which is the amount charged to you when you buy or sell an investment. If you change too often, these can eat into your total return.

3. You may lose sight of your risks

Different investment options may have completely different objectives and risk levels. If your objectives align with Fund A and you switch to Fund B because it did better last year, you may be taking on more risk than you realise.

Returns can’t be considered in isolation – it’s important to also consider the amount of risk. A high-risk investment might experience very high returns, but it may also be more likely experience a negative return. A risk averse investor can easily get themselves into trouble if they switch into a high-risk and high potential return option after a period of strong performance.

For example, earlier we mentioned our investor named Doug invested in tech shares at the beginning of 2000. Shares are considered a higher risk investment, but Doug had several large expenses coming up in the year 2001, and so was not able to afford a sudden, large decline in the value of his investment.

So, when tech shares dropped over 40% in 2000, that meant that Doug’s original $50k investment dropped below $30k in just one year. Doug had taken on more risk than he could afford at the time and that risk did not pay off when the investment did not provide any returns, but instead created additional financial stress.

With higher risk options, like shares, there may be the potential for higher returns but it’s important that investors also consider any associated risks, including their tolerance to ride out any potential down periods.

Take a long-term view

If only picking investments was as easy as picking last year’s winner. Many other factors – including fees, risk, management quality, fund objectives, and your personal objectives – need to be taken into account before you make investment decisions. If you’re not sure, talk to a professional financial adviser who can help tailor investments to suit your situation.

Need help?

Choosing how you invest your super could make a difference to how much money you have in retirement. To help you make the right choice, use our Investment Choice Solution tool to see what kind of investments might suit you.

Diversification: why is it important for your super?

A simple guide to help you understand the potential benefits of diversification, why it matters to your super and what a diversified portfolio might look like.

Learn more about shares and why they can play an important part in your super. This article explains how Rest may use shares to help grow your super faster.