What an interesting start to 2023 we’ve had. While it’s only April, it certainly feels like investment markets have already packed plenty in.

Stepping away from the desk, a highlight for me so far this year was our Annual Members Meeting in February. It was a welcome change meeting some of our members in person as well as over zoom and answering your questions on everything from our investment strategy to our approach to sustainability.

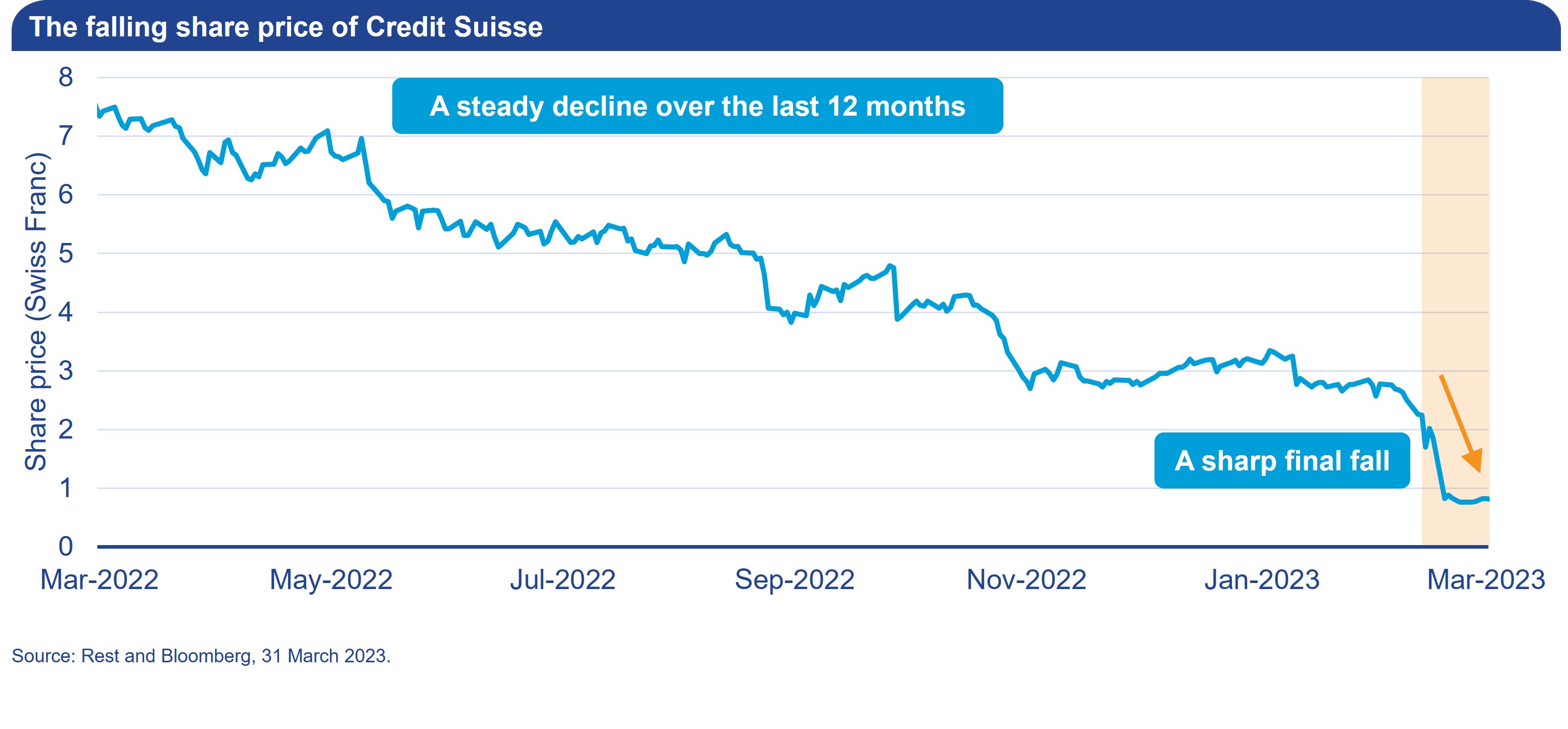

Looking at markets, we understand that the headlines on the US regional banks and Credit Suisse may be unsettling for many of you. It was undoubtedly a bumpy period for share markets, but fortunately we saw some calm as regulators intervened.

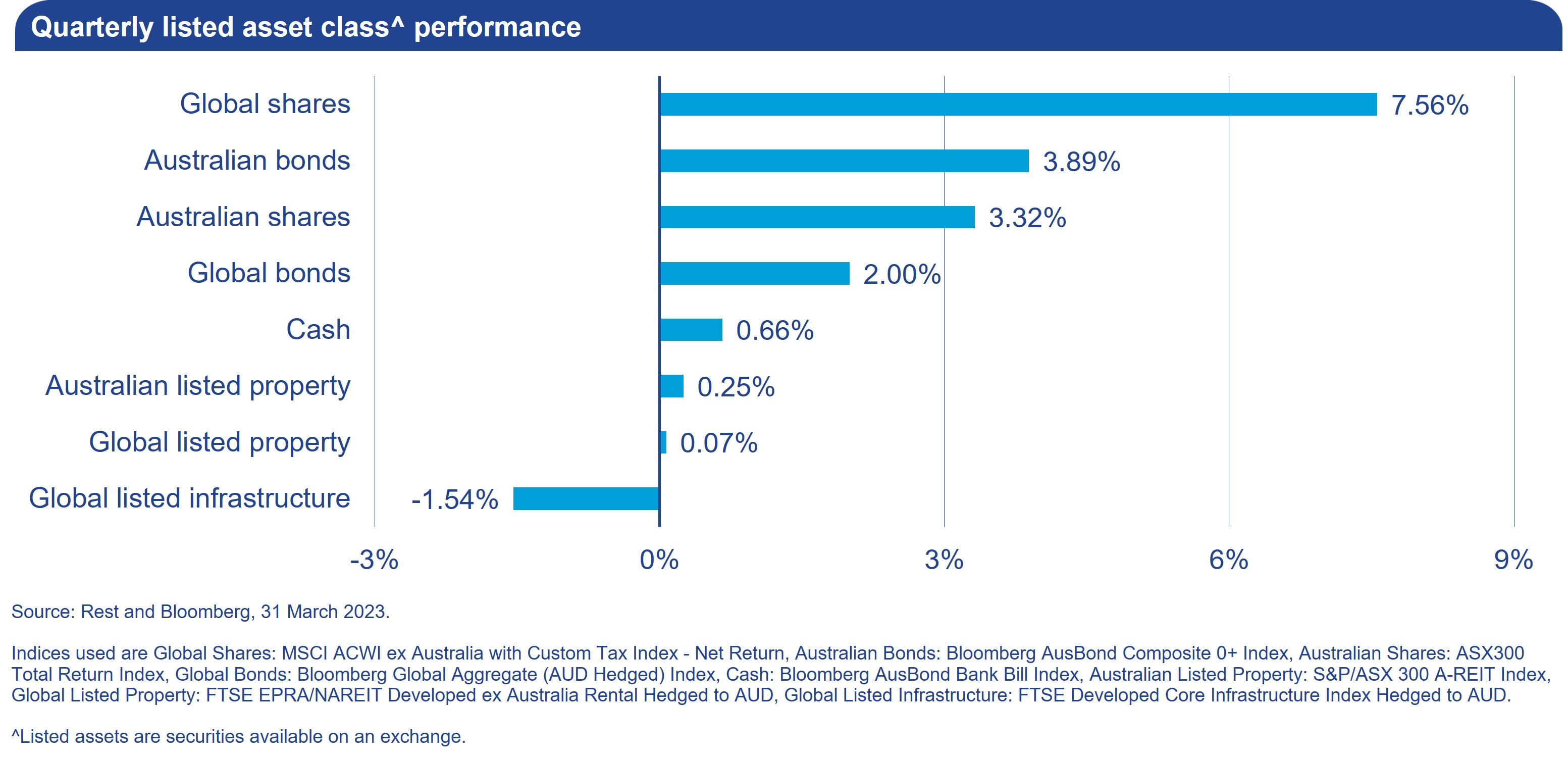

| 3 months (%) | Financial YTD (%) | 10 years (% p.a.) |

|---|---|---|

| 2.36 | 5.67 | 7.28 |

| 3 months (%) | 2.36 |

| Financial YTD (%) | 5.67 |

| 10 years (% p.a.) | 7.28 |

| 3 months (%) | Financial YTD (%) | 10 years (% p.a.) |

|---|---|---|

| 2.16 | 5.10 | 6.74 |

| 3 months (%) | 2.16 |

| Financial YTD (%) | 5.10 |

| 10 years (% p.a.) | 6.74 |

The Banking Brief

Skip ahead to read about the Australian banks and what this all means for your super

Born in the USA

It all started with the US regional banks. In early March, SVB became the largest US bank to collapse since the gloomy days of the 2008 global financial crisis (GFC). We know we talk about the importance of diversification a lot, and the failure of SVB highlights again why diversification matters – it’s not limited to just super investments!

As the name Silicon Valley suggests, the bank’s customer base was focused on tech startups. This meant that a large chunk of the deposits held at SVB were from just this industry.

Over the last 12 months, rising interest rates have caused a lot of pain for these startups as they received less funding from investors. This has meant that many startup companies have needed to withdraw their deposit money from banks to cover expenses. Unfortunately for SVB though, as their customer base was very concentrated, many customers withdrew their deposit money at the same time (otherwise known as a ‘bank run’). So, just like when you are investing, a lack of diversification does mean more concentration risk.

A bank run can be very problematic as banks often have this deposit money tied up in other investments and they can’t return it easily when a lot is requested at once. This led to significant financial losses for SVB and ultimately its demise.

Two other smaller regional banks (Silvergate Capital Corp and Signature Bank) also announced they would be winding up operations within that same week. As with SVB, these banks had a poorly diversified customer base and were major banks for cryptocurrency companies. So again, the lack of diversification left these regional banks very vulnerable to a bank run if cryptocurrency markets struggled (newsflash: they did). These banks therefore also failed as they were unable to meet the demand for deposit money.

The US Federal Reserve has now stepped in to guarantee bank deposits at SVB and Signature, providing some comfort to both their customers and markets.

Investment Updates

Diversification and why it matters to super

The recent turmoil in financial markets offers a timely reminder of the benefits of diversification.

Investment Updates

Investing in volatile times

Make sure you’re comfortable your investment option's risk profile and give markets time to recover.

General

Risk and return in your super investments

Investments involve risk including super. Learn about risks to consider before investing your super.